Critical Minerals in Pakistan are a point of concern around the world amid the growing global escalations when Strait of Hormuz is blocked. Critical minerals are a group of natural resources essential for the functioning of modern technologies, especially in renewable energy systems, electric vehicles (EVs), and advanced electronics. These minerals include lithium, copper, cobalt, nickel, and rare earth elements (REEs), which are vital for battery storage, wind turbines, semiconductors, and defense applications. The global shift toward low-carbon energy systems has greatly increased the strategic importance of these minerals.

As nations strive to cut carbon emissions and expand clean energy infrastructure, demand for critical minerals is surging at an unprecedented rate. Thus, securing reliable and diversified supply chains has become a major concern for both developed and emerging economies. In this context, resource-rich countries with underdeveloped mining sectors are gaining attention. Pakistan, with its considerable yet underexplored mineral reserves, is increasingly seen as a potential contributor to global mineral supply chains.

Global Context: Demand, Supply, and Strategic Competition

The global demand for critical minerals is expected to grow significantly over the coming decades. According to the International Energy Agency (IEA), lithium demand could increase by more than six times by 2040 under a net-zero emissions scenario, while demand for copper and rare earth elements is projected to double or triple due to their extensive use in renewable energy technologies and electric mobility systems. Despite rising demand, the global supply of critical minerals remains highly concentrated. China currently dominates the processing and refining of rare earth elements, accounting for approximately 60-70% of global rare earth processing capacity, according to various international energy assessments.

Similarly, lithium production is concentrated in countries such as Australia, Chile, and Argentina, while the Democratic Republic of Congo (DRC) produces nearly 70% of the world’s cobalt. This concentration has raised concerns about supply chain vulnerabilities and geopolitical risks. The United States, the European Union, and other advanced economies have increasingly emphasized the need to diversify supply chains and reduce dependence on a limited number of suppliers. This shift has opened new opportunities for emerging mineral-producing countries.

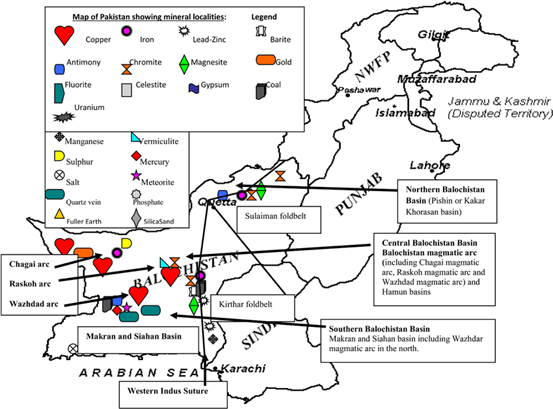

Pakistan’s Mineral Potential

Pakistan possesses significant mineral resources, particularly in Balochistan, Gilgit-Baltistan, and Khyber Pakhtunkhwa, although much of this potential remains under explored. One of the most prominent projects is the Reko Diq copper-gold deposit, located in the Chagai district of Balochistan. According to estimates by Barrick Gold and Pakistan’s Ministry of Energy, Reko Diq contains approximately 5.9 billion tons of ore, making it one of the largest undeveloped copper-gold deposits in the world.

The Saindak copper-gold project, also located in Balochistan, has been operational for several years, contributing to Pakistan’s mineral output. However, its production levels remain relatively modest compared to global standards, reflecting broader challenges in the sector. In addition, geological surveys indicate the presence of untapped mineral belts in northern Pakistan, including potential deposits of rare earth elements and other industrial minerals.

Despite these resources, according to the Pakistan Economic Survey, Pakistan’s mining sector contributes only around 2-3% to the national GDP.

This indicates a significant gap between resource availability and economic utilization. Limited exploration activities, outdated technology, and insufficient investment have constrained the development of the sector.

Economic and Strategic Importance

The development of Pakistan’s critical mineral sector has the potential to significantly contribute to economic growth. Increased mining activity can boost export revenues, create employment opportunities, and stimulate industrial development. Furthermore, integrating mineral development with infrastructure initiatives such as the China-Pakistan Economic Corridor (CPEC) could improve connectivity and facilitate the transportation of resources to domestic and international markets. From a strategic perspective, critical minerals are increasingly viewed as instruments of economic and geopolitical leverage. As global competition intensifies over access to these resources, countries with mineral reserves gain greater importance in international supply chains. Pakistan’s geographic location and resource base position it as a potential partner for countries seeking to diversify their mineral sources.

According to analysis by the World Bank, countries that successfully develop their mineral sectors can significantly benefit from the global energy transition, provided they invest in governance, infrastructure, and value-added processing. In Pakistan’s case, moving beyond raw material exports toward refining and processing could enhance long-term economic gains and reduce dependency on external markets.

Stakeholder Perspectives

Stakeholder perspectives highlight both the opportunities and challenges within Pakistan’s mineral sector. Government authorities have increasingly emphasized the need to attract foreign investment and modernize mining regulations to unlock the country’s mineral potential. Recent developments surrounding the revival of the Reko Diq project reflect a renewed policy focus on large-scale mining initiatives.

Experts and analysts, however, point to structural limitations that continue to hinder progress. According to reports by the World Bank and the Sustainable Development Policy Institute (SDPI), Pakistan’s mineral sector remains underdeveloped due to limited geological exploration, weak institutional capacity, and regulatory inconsistencies.

Academic and industry experts also stress the importance of sustainability and governance. Studies in resource governance indicate that without transparent regulatory frameworks and community engagement, large-scale mining projects may face environmental and social challenges. Analysts in energy and resource governance note that Pakistan’s mineral potential is substantial, but realizing this potential requires long-term policy consistency, technological investment, and institutional strengthening.

Challenges and Constraints

Despite its significant mineral potential, Pakistan faces multiple structural challenges that hinder the development of its mining sector. One of the primary issues is the lack of comprehensive geological exploration. Large areas of mineral-rich regions remain underexplored due to limited technological capacity and insufficient investment in modern survey techniques.

Another critical constraint is the regulatory and institutional framework. According to the World Bank, inconsistent policies, bureaucratic delays, and lack of coordination between federal and provincial authorities have discouraged foreign investment in the mining sector. These governance issues create uncertainty for multinational companies seeking long-term investments. Infrastructure limitations also pose a major barrier. Many mineral-rich areas, particularly in Balochistan, lack adequate transportation networks, energy supply, and water resources necessary for large-scale mining operations. This significantly increases operational costs and reduces competitiveness.

Environmental and social issues make it harder to develop minerals. If not handled well, mining can cause damage to land, reduce water availability, and push local people out of their homes. Experts in sustainable development say that poor environmental rules can harm both the economy and society. According to studies by the Sustainable Development Policy Institute (SDPI), solving these problems needs changes in how institutions work, more money for new technology, and using mining methods that follow global standards.

Policy and Development Initiatives

In recent years, Pakistan has taken steps to improve its mineral sector. One big change is the restart of the Reko Diq project, which came after an agreement that allowed for new foreign investments. This project is expected to bring in billions of dollars and provide long-lasting economic benefits. The government is also looking to change mining rules to make it easier for investors. Plans are being made at both the national and regional levels to make the licensing process smoother, increase openness, and improve the ability of government agencies to manage things.

Additionally, Pakistan is trying to connect its mineral industry with bigger economic plans, like the China-Pakistan Economic Corridor (CPEC). Better roads and transport under CPEC could help extract, process, and export minerals by linking areas with resources to ports. Working with other countries is another area of focus. Pakistan is talking to foreign partners to get investment and technical help in mining and mineral processing. According to the World Bank, countries that work well with others are better at building strong, sustainable mineral industries.

Comparative Perspective: Pakistan and Global Leaders

When compared to top mineral-producing countries like Chile and Australia, Pakistan lags behind. Chile is one of the world’s biggest producers of lithium and has a strong set of rules that encourage foreign investment while protecting the environment. Australia is a global leader in mining due to advanced technology, clear rules, and good infrastructure. In contrast, Pakistan’s mineral sector is still underdeveloped even though it has similar resources. While Chile and Australia have linked their mining industries to global markets, Pakistan mainly exports raw materials. However, this gap is also an opportunity.

By learning from countries like Chile and Australia, such as having clear rules, welcoming investments, and using modern technology, Pakistan can become more competitive in the global mineral market. This comparison shows the importance of having good institutions, strong governance, and long-term planning to turn resource potential into economic and strategic benefits.

Conclusion

Pakistan has a lot of untapped reserves of important minerals that are key in the shift to clean energy and new technologies. While the world needs these resources more than ever, the country’s mineral sector is still underdeveloped due to problems with structure, rules, and infrastructure. Recent changes, such as the restart of important mining projects and more attention from policymakers, show a move toward better use of these resources. But to fully use this potential, Pakistan needs ongoing work to improve government systems, bring in investments, and use modern technology.

The formation of Special Investment Facilitation Council may be a step in the right direction. However, a balanced approach that includes economic growth, protecting the environment, and working with other countries will be key for Pakistan to become a serious player in global mineral supply chains.